On the 21st November S&P moved its ‘A+’ rating for SCOR’s core carriers to a positive outlook. A return to the ‘AA’ range would highlight the remarkable transformation of the group’s profile from the difficult position it found itself in a decade ago.

SCOR’s path to recovery is well documented but the assignment of the highest Enterprise Risk Management (ERM) assessment from S&P (‘very strong’) is a rare accolade.

Only 5 other reinsurance groups achieve this (Aspen, Hannover Re, Munich Re, Renaissance Re and Swiss Re). Moreover only two European primary groups also achieve this, Allianz and RSA, and RSA’s assessment is under some pressure following recent surprise losses at the group.

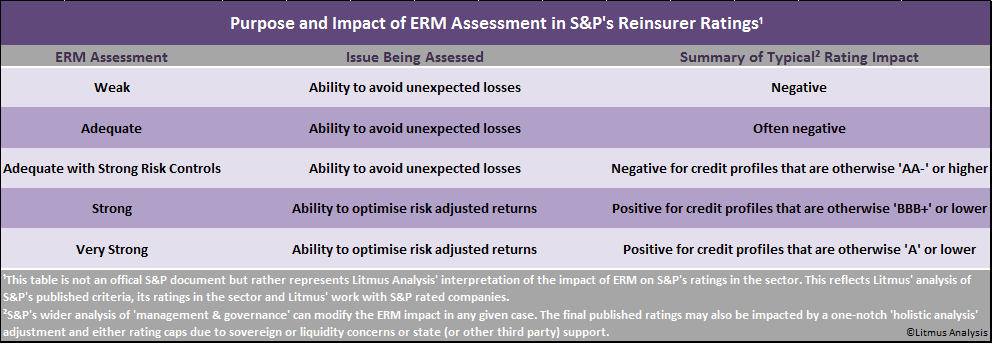

S&P’s ERM assessment scale has 5 categories and we summarise the potential ratings impact below –

(For a high resolution of this chart, email us – info@litmusanalysis.com).

While analysis of ERM is a detailed and jargon filled subject (S&P maintains a specialist team to support its work in this area) the principles behind the assessments are actually straightforward.

The first step is an evaluation as to whether the organisation has the systems in place to avoid nasty surprises relative to its Risk Appetite (hence the pressure on the RSA assessment). The important point here is that it is not a judgement of how ‘risky’ the Risk Appetite actually is; simply whether, having defined it, the re/insurer can manage according to that appetite. ‘High risk’ re/insurers can have a ‘very strong’ ERM assessment and ‘low risk’ re/ insurers can have a ‘weak’ ERM assessment.

A ‘weak’ assessment derives from either a lack of a properly defined Risk Appetite or S&P’s belief that the systems in place are insufficiently strong to reliably operate within that appetite. We will not dwell on the details of the analysis here but issues looked at include the controls in place, the quality and usage of models and the overall ‘risk culture’ of the organisation.

In theory, without external support, a reinsurer assessed as ‘weak’ for ERM could achieve only a BBB+ rating at best even if the rest of its profile was extremely strong (without external support).

The ‘adequate’ and ‘adequate with strong risk controls’ assessments both indicate S&P’s belief that the Risk Appetite should be achievable (the latter usually reflecting sectors, such as reinsurance, where the risk control environment is more challenging, thereby requiring more robust systems). However, given the importance the agency places on ERM within the reinsurance sector, a reinsurer achieving just the ‘adequate’ assessment needs to do well in the wider ‘management & governance’ part of the analysis not to risk having its rating lowered due to ERM.

The two highest assessments by contrast relate to how a rated group’s ERM will positively enhance its risk-adjusted performance. In essence this means how the systems in place AND the strategic use of ERM allow the maximisation of return for any defined Risk Appetite. Part of this is a rare example of a rating agency embracing the idea of opportunistic behaviour; albeit in the context of highly sophisticated systems allowing this to be done optimally.

To achieve either of the two top categories the rated group first needs to demonstrate it has an effective process in place for evaluating and then managing ‘emerging risks’. Thereafter the ‘strong’ category reflects a holistic approach to risk/return optimisation. Leadership decisions across issues such as line of business prioritisation, investment policies, diversification strategies and other areas, along with successful execution, are at the heart of this.

Finally to achieve the ‘very strong’ category, the group’s internal economic capital model needs to score highly as the underlying management tool for the above (this in itself requires a separate analysis by the agency).

The direct and indirect impact of a ‘strong’ or ‘very strong’ ERM assessment on a reinsurer’s rating can be very significant. Catlin’s ‘A’ rating is fundamentally driven by both its ‘strong’ ERM score and its risk-adjusted out-performance (seen as derived from its strong ERM). Partner Re by contrast, with an otherwise ‘AA-‘ profile, is actually rated lower than this implies at A+; were its ERM assessment to be ‘strong’ rather than ‘adequate with strong risk controls’ the rating would very probably be ‘AA-‘.

For SCOR the move to ‘very strong’ for its ERM does not in itself increase its A+ rating. However, S&P’s faith in the quality of SCOR’s ERM is reflected in the agency’s belief that the consequent earnings performance will bolster and sustain capital adequacy such that a ‘AA-‘ rating becomes merited.

Stuart Shipperlee, Analytical MD, Litmus Analysis

Leave a Reply