Litmus Analysis’ Reinsurance Renewal Roundup – January 2022

An examination of the P&C treaty renewals of the big four European reinsurance groups

Lewis Phillips

Consultant Analyst

Lucy Stupples

Consultant Analyst

Introduction and Executive Summary

The big four European reinsurers (Hannover Re, Munich Re, SCOR and Swiss Re) together represent around one third of global P&C reinsurance premiums, and their January renewals encompass close to half of their traditional treaty reinsurance premiums.

In essence acting as a bellwether for the market as a whole, these groups tend provide more detail than their Bermudian and international peers, their experience acting as a useful indicator for the market as a whole. In addition to commenting on their individual experience, Litmus uses their disclosures to present a composite picture.

- 1st January 2022 renewals presented a more consistent picture than at the previous year, with each company growing its renewed book

- Once again, different priorities were reflected in the individual outcomes at renewal

- Strong demand from cedants and higher pricing generated 10% volume growth in the combined portfolio at renewal, compared with 5% achieved last year

- There was strong new business growth across almost all core business lines

- Risk-adjusted pricing firmed overall, as price increases were achieved on almost all lines and territories – especially on loss-affected business

- Economic profitability of new business was said to have improved, in part due to rising interest rates

- Each of the companies also expects these favourable trends to continue through subsequent 2022 renewals

The ‘Big Four’ global reinsurers see firming conditions at January 2022 renewals as an opportunity for growth

The four largest European reinsurance groups took advantage of attractive market conditions to grow their book at the recent 1 January 2022 treaty renewals. Results were more consistent than in previous years, with each company reporting higher premium volume at renewal. In aggregate, the combined book grew by 10%, ranging from Swiss Re’s 6% to 14% for Munich Re.

1 January is an important date in the reinsurance industry’s calendar, as the renewal date for the bulk of European P&C treaties and much other business around the world. All the major reinsurers provide some commentary on their January renewals, but the big four European reinsurers (Hannover Re, Munich Re, SCOR and Swiss Re, who together represent around one third of global P&C reinsurance premiums) provide more detail than their Bermudian and international peers. In this brief report, we examine the public disclosures from these companies, and have aggregated the four to present a composite picture.

For this group, around half of traditional treaty reinsurance premiums were up for renewal at 1 January 2022. Other important dates are 1 April (when Japanese and other Asian business renews), 1 June (Florida cat) and 1 July (some US, Australasia, and other global programmes). Facultative and specialty business have no common renewal dates and are spread throughout the year.

Sources: Company disclosures. Swiss Re reports in US dollars; for the purpose of this aggregation, its figures have been converted into euros using the 1 January 2022 exchange rate of USD 1 = EUR 0.885

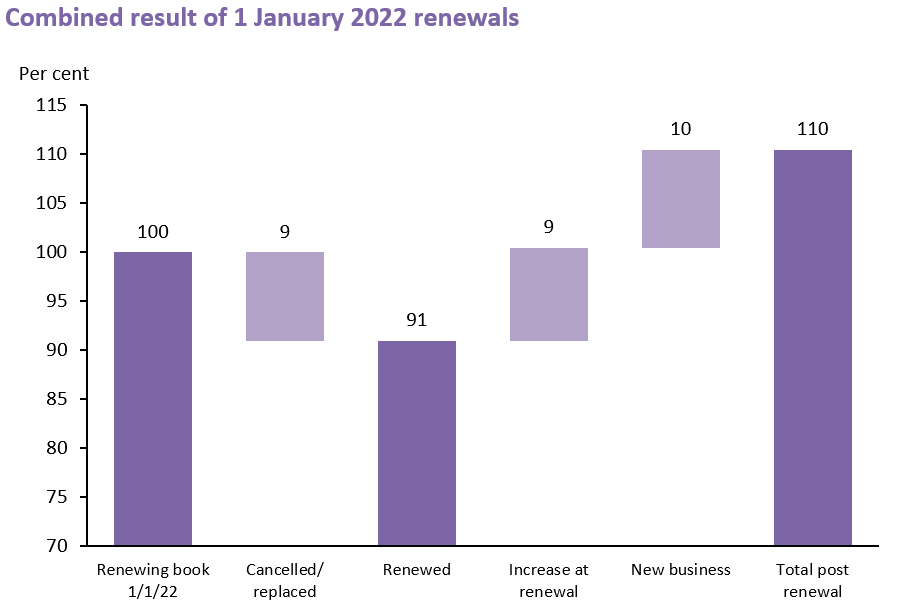

We have combined the reported renewal experience of the four groups, and the overall picture is shown above.

The development of the renewal is shown in the top waterfall chart. EUR 31.9bn of treaty reinsurance premiums were up for renewal. Of this 9% was cancelled or replaced (which includes reductions in shares on renewing treaties as well as business declined and not renewed), giving a total of EUR 29.1bn which was renewed. The 9% increase at renewal represents both the effect of price changes and increases in shares on treaties. New business contributed an additional 10%, benefiting from growth across virtually all core business lines. The combined portfolios grew 10% to EUR 35.3bn, compared with 5% growth reported at 1 January 2021. In aggregate, the weighted average price increase was 2.7%.

Each of the companies in our study reported an overall increase in risk-adjusted pricing, ranging from 0.7% for Munich Re to 4.9% for SCOR (1.1.2021 range: 2.4% for Munich Re, to 7.8% for SCOR), with price increases across almost all lines and territories, especially on loss-affected business. Terms and conditions were said to have tightened.

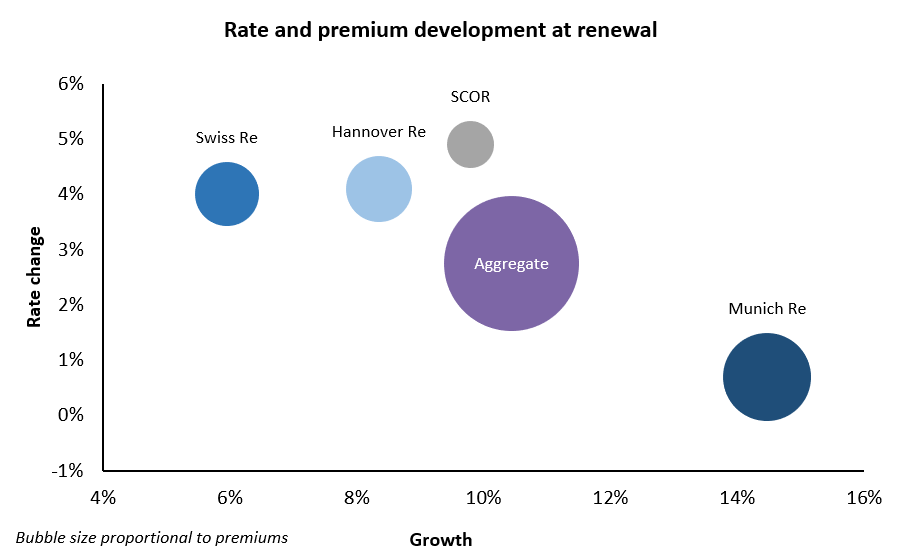

The bubble chart shows the overall rate and premium development at renewal reported by the four companies. Munich Re reported the highest increase in premium volume, up 14%, with strong but selective growth in a firming market. At the other end of the range, Swiss Re’s increase was a more modest 6%, which it termed “attractive”, as it continued to focus on underwriting quality.

SCOR reported an underlying increase in renewed premiums of 10% (excluding one large non-recurring transaction) which was driven by growth in its Global Lines segment; Hannover Re’s renewed book increased by 8% with growth achieved in almost all regions and classes of business.

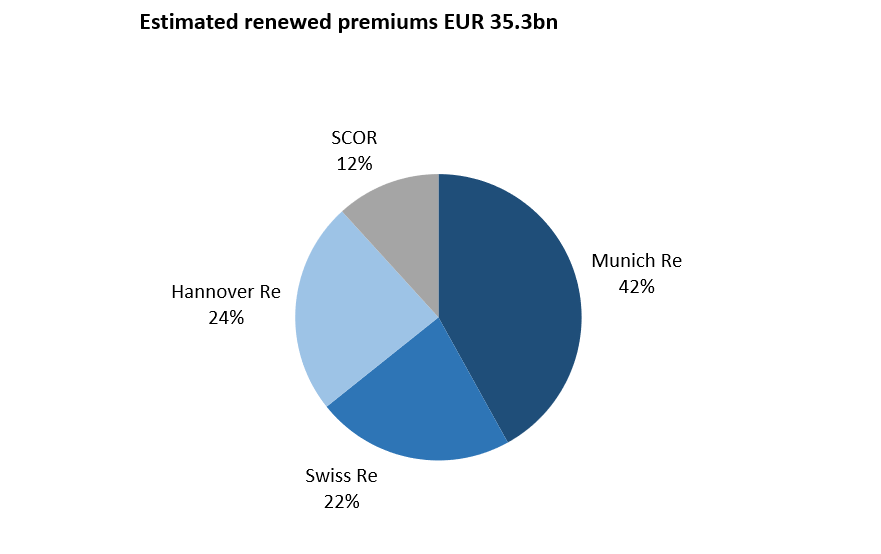

The pie chart shows the distribution of the EUR35.3bn of renewed premium across the four groups.

Each of the companies in our study commented that the favourable trends experienced at the January renewals were expected to continue through the later renewals during the year. Rising interest rates were noted as a contributor to increased economic profitability of new business.

Hannover Re

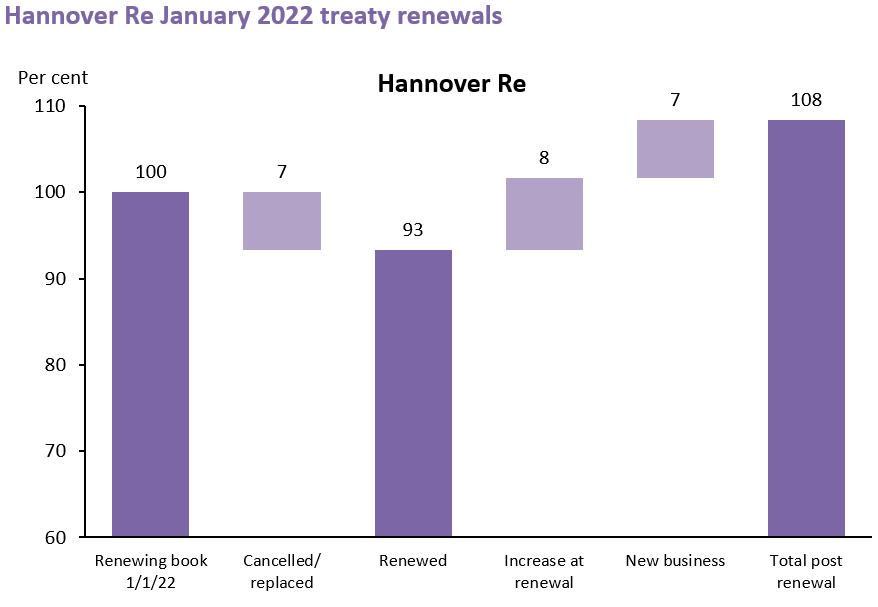

Hannover Re had EUR 7.8bn of traditional treaty reinsurance premiums up for renewal at 1 January 2022, representing 62% of its total book (following Hannover Re’s sale of its participation in HDI Global Specialty, a mandatory cession from this company is excluded, as is structured reinsurance, ILS and facultative business). A further EUR 4.9bn of traditional treaty business is due to renew later in the year. 43% of renewing business came from Europe, Middle East and Africa (EMEA), 25% from the Americas, and 16% from the Asia Pacific region, with the remainder comprising global specialty business. The company pointed to a fifth consecutive year of improving conditions in the reinsurance markets with positive pricing momentum sustained in many areas.

Hannover Re’s treaty renewal generated an 8% increase in premiums, adjusted for exchange rate movements, compared to a 9% growth at the 1 January 2021 renewal. The increase was driven by price rises, larger shares on existing business and substantial new business. Premiums grew by 3% on renewed proportional business and by 13% on non-proportional.

The chart below shows the outcome, in terms of premium growth, for each company and the aggregate at each of the major renewal periods over the last two years. At mid-year 2021, each company reported an increase in renewed premiums, while growth was more muted, and negative for Swiss Re, in the same period for 2020.

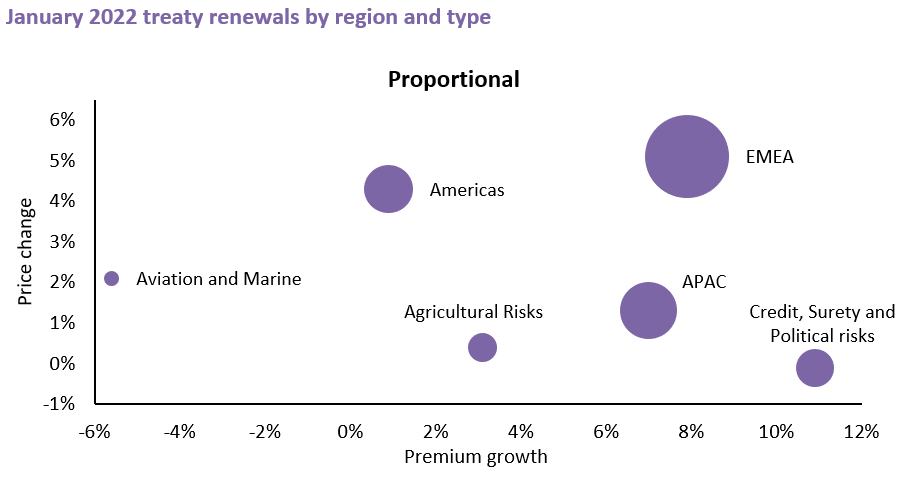

Hannover Re reported growth in renewed premium across all major markets/business lines. The increase across the major regions ranged from 10% in EMEA to 7% in the Americas. Growth in global specialty lines ranged from 11% in Credit, Surety and Political Risks, to 1% in Aviation and Marine.

The 10% increase in premium volume in EMEA was mainly a function of price increases, notably on cat-affected programmes, as well as a strengthened market position in Germany, and increased capacity in a hardening market at Lloyd’s.

Business in the Americas grew by 7%, where a moderate expansion in casualty more than offset selective reductions in proportional property. There was also a benefit from firmer prices, notably in Cyber.

APAC business volume increased by 8% with new business gains in South-East Asia, which was partly offset by reductions on Chinese proportional treaties where margin requirements were not met. Low loss activity in the region tempered the positive pricing momentum.

Credit, Surety and Political Risks premiums rose by 11%, driven by post-pandemic economic recovery and the winding down of state guarantees. Low loss activity again limited price increases.

Aviation and Marine premiums increased by just 1% against a backdrop of low flight activity.

Agriculture business grew 3%, mainly as a result of positive pricing trends and selective growth in regions such as Brazil.

On its total renewed book, Hannover Re achieved an average price increase of 4.1%, compared with 5.5% at 1 January 2021. Following heavy catastrophe losses in 2021, cat price rises were a major driver. Price increases were obtained across all major regions and classes, ranging from 1% in APAC and Credit, Surety and Political Risks, to 5% in EMEA, the Americas and Aviation and Marine.

Pricing on proportional business (71% of renewed premiums) was up 3.4%, while non-proportional pricing improved by 6.1%. The main drivers of price increases were said to be the interest rate environment, loss experience, and inflation. Conditions were stable to slightly improved.

The treaty renewals exclude EUR 1.1bn of facultative reinsurance premiums and EUR4.5bn of structured reinsurance and ILS transactions, all of which renew throughout the year, as well as EUR1.1bn related to the mandatory cession from HDI Global Specialty; following the sale of Hannover Re’s participation, this cession was reduced, as planned to EUR 576mn.

Commenting on structured reinsurance, Hannover Re pointed to continuing high demand for tailor-made capital management transactions and solutions for commercial short-tail and personal lines in the US. Demand for facultative reinsurance remains high, and Hannover Re said it benefited from a flight to quality among buyers. Market conditions continued to harden across most lines of business and regions, with an average rate increase of 5% achieved.

Heavy catastrophe loss activity during the preceding year generated strong demand for cat. protections, with an average 6.6% risk-adjusted price increase achieved.

Munich Re

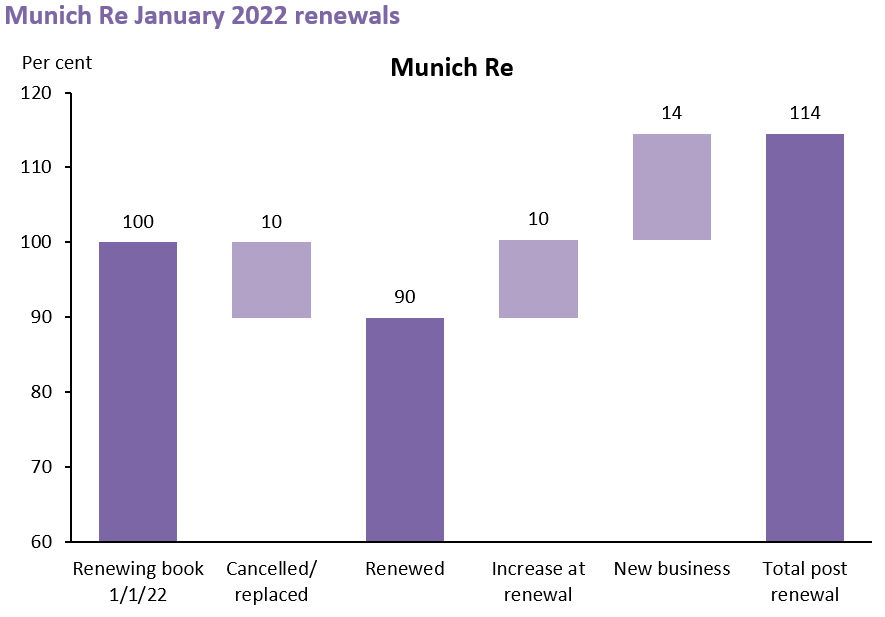

Some 45% of Munich Re’s total P&C reinsurance book was up for renewal at 1 January 2022, with a focus on Europe and North America (mainly excluding hurricane cover which renews later in the year), together comprising around two thirds of the renewing book, with the remainder from Asia Pacific and Africa, and worldwide business.

EUR 12.9bn of premium was up for renewal, and the book grew by 14%, compared to an increase of 11% at the 1 January 2021 renewal, resulting in EUR 14.8bn of renewed premiums. Natural Catastrophe was 11% of the renewing book. Renewed premium increased in all major classes.

Munich Re reported an average risk-adjusted price increase of 0.7% across its renewed book (1.1.2021: 2.4%), with terms and conditions generally improved. Contributory drivers at the renewal were high catastrophe losses during 2021, low interest rates and inflationary pressures, and increased risk-awareness among cedants with a “flight to quality” in evidence. Munich Re also pointed to a tightening of alternative capacity.

Munich Re continued its strategy of selective growth. It sought to limit exposures in certain natural catastrophe business, with an unchanged share from this class, while it grew its book of structured quota share business.

As in the previous year, price increases were achieved across all major classes and territories. Prices hardened in Europe, particularly in loss-affected business (e.g. Germany), with additional upward pressure from low interest rates and increasing inflation. It obtained strong nominal rate increases across the book in North America, reflecting catastrophe loss experience, and Casualty lines which were affected by inflation. Price increases were tempered by more cautious loss assumptions leading to only a slight improvement in risk-adjusted pricing. Price increases were achieved in loss-affected business in Asia Pacifica and Africa, but prices were broadly stable in other lines across the region. Worldwide Specialty represented a little over a quarter of the renewed book, with overall risk-adjusted pricing largely flat.

Munich Re noted it had achieved profitable growth across all regions and perils at this renewal.

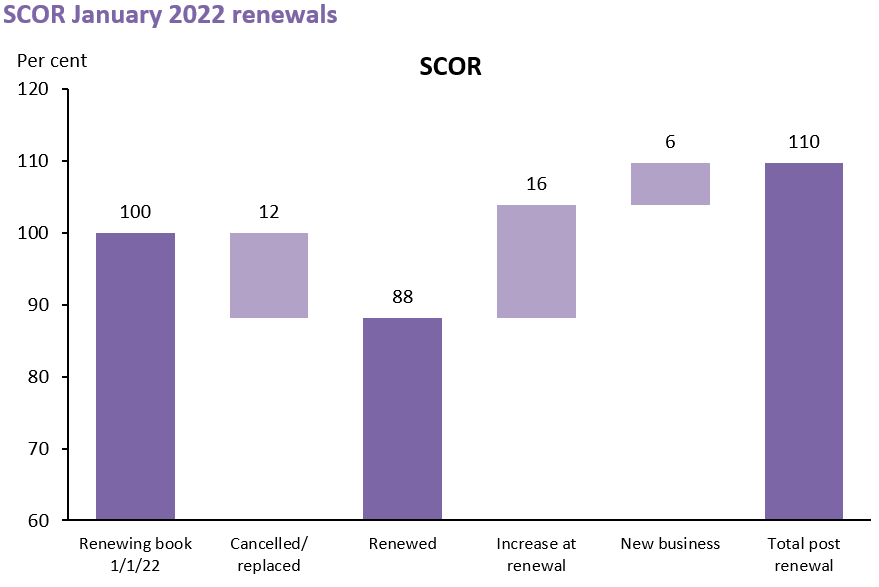

SCOR

The emphasis for SCOR at the 1 January 2022 renewal was portfolio management, as it took advantage of favourable conditions to expand its profitable Global Lines book, while modestly reducing its catastrophe book (notably in the US) and rebalancing the Property & Casualty lines.

Overall, around 64% of SCOR’s treaty reinsurance book was up for renewal, with 83% of the European portfolio renewing, 50% of the North America book, 36% of Mature Asia-Pacific and 62% of Fast Growth Markets. Excluding a non-recurring large European structured transaction, a total of EUR 2.6bn of P&C Lines premiums and a further EUR 1.9bn of Global Lines was subject to renewal, giving a total of EUR 3.8bn of renewing premiums. Renewed volume in P&C Lines was EUR 2.7bn, an increase of 5%, while Global Lines premium volume grew by 21% to EUR 1.4bn. The overall result was a 10% increase in renewed premium volume to EUR 4.1bn, compared with a 16% increase to EUR 3.4bn at the 1 January 2021 renewal. Including the large structured transaction, renewed premiums were up 19%. The large increase in Global Lines was tempered by a smaller increase in the Property & Casualty lines, where SCOR continued to optimise the book. Growth came principally from Europe and Fast Growth Markets, while there was a reduction in the US and APAC Mature Markets divisions.

P&C lines include: Property, Property Cat, Casualty, Motor and other related lines; Global lines include: Agriculture, Aviation, Credit & Surety, Inherent Defects Insurance, Engineering, Marine and Offshore, Space, Cyber, Motor Extended Warranty and inwards Retro.

APAC Mature Markets comprise Australia / New Zealand, Japan and South Korea.

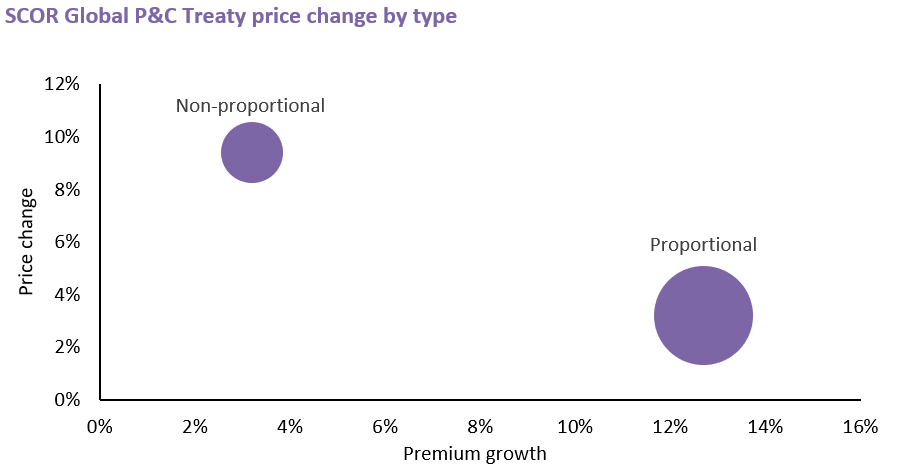

Proportional P&C treaty premium volume was up 13% with an average price increase of 3.2% while non-proportional treaty premiums grew 3% with pricing up 9.4% on average.

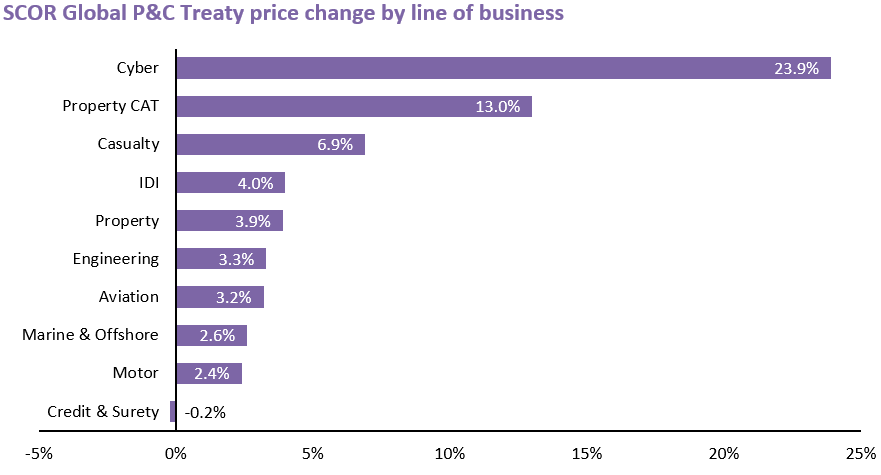

SCOR reported price increases across almost all business lines, ranging from 2.4% in Motor to 23.9% in Cyber. The exception was Credit & Surety where average risk-adjusted pricing declined by 0.2%. Overall, pricing increased by an average of 4.9%.

Premium volume in Global Lines business grew 21% with an average price increase of 2.9%. Growth was focused on segments where conditions and rate adequacy were deemed most favourable, particularly Credit & Surety, Marine & Energy.

In P&C lines (non-cat.), premium volume increased 6% with an average price increase of 4.4%. Growth came principally from Europe, notably on Casualty as well as Motor.

Portfolio management was a feature of the Property Cat renewal as SCOR rebalanced its book, noting that, in some markets, price rises on cat-exposed business were still insufficient to meet margin targets after retrocession costs. Consequently, SCOR repositioned its book in North America, including exiting from US primary wind-exposed MGA business, leading to a reduction of 11% in SCOR’s 1-in-250 cat. net projected probable maximum loss.

Commenting on its Specialty Insurance business, which has no set renewal dates, SCOR reported an average premium growth through 2021 of 19% with an average price increase of 12.6%. Property Lines saw rate increases throughout the year, but slowing to single digits percentage increase towards the end of the year. Energy rates rose through the year, with some stabilisation by the end. Casualty and Financial Lines saw continuing rate momentum, in part driven by social inflation. There was also very strong hardening (69%) in Cyber.

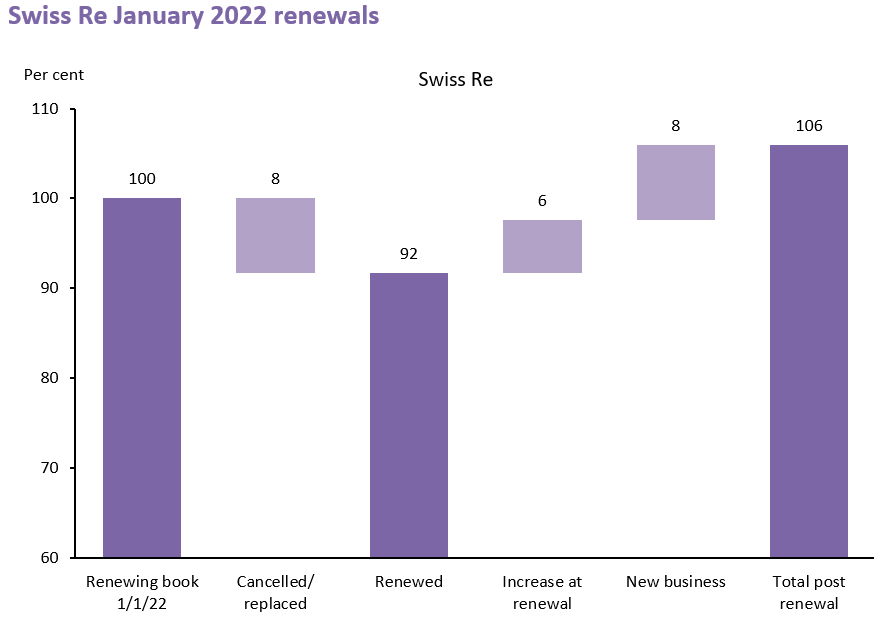

Swiss Re

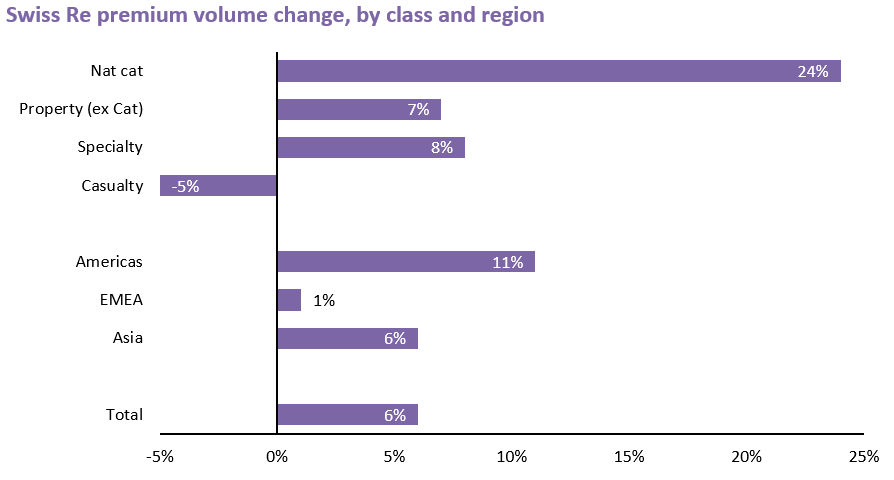

46% of Swiss Re’s treaty reinsurance business renewed at 1 January 2022, with USD 8.4bn of premiums up for renewal (excluding USD 1.6bn of business reported on a deposit account basis and USD 0.8bn of facultative reinsurance business).

Business falling short of return targets, particularly in Casualty, was cancelled and not replaced, but Swiss Re noted good opportunities for growth in other areas which did meet its targets. With a continued focus on underwriting quality and selective growth, the overall result was a 6% increase in renewed premiums to USD 7.8bn, in contrast to a reduction of 11% in renewed premiums reported at 1 January 2021.

Swiss Re reported an overall 4% price increase across its renewed book. This was said to offset more conservative loss assumptions, which reflect a prudent view on inflation and other changes in exposure.

Strong growth was achieved in property and specialty lines. Natural catastrophe-related premium volume were up by 24%, with targeted growth mainly in EMEA and the USA and a cautious approach to low-attaching aggregate covers. Growth in Specialty was largely driven by rate improvements in Credit & Surety and positive momentum in Cyber. A 5% reduction in Casualty lines was attributed to a reduction in low-margin EMEA motor business.

Significant price increases were achieved on Property in loss-affected regions, although the increase was partly offset by higher modelled loss assumptions. Price increases were more modest in loss-free regions. There was positive pricing momentum in Specialty lines, especially Cyber, Engineering and Credit and Surety.

For any further information please contact analytics@litmusanalysis.com

Leave a Reply