An examination of the P&C treaty renewals of the big four European reinsurance groups

Lewis Phillips

Consultant Analyst

Lucy Stupples

Consultant Analyst

The big four European reinsurance groups reported divergent results from the 1 January 2020 renewals. The change in renewed premiums varied from +14% for Hannover Re to a contraction of 6% for SCOR. While all reported an overall increase in risk-adjusted pricing, the change ranged from 1% for Munich Re to 5% for Swiss Re.

As the renewal date for the bulk of European P&C reinsurance treaties and much other business around the world, 1 January is a very important date in the industry’s calendar. All the major reinsurers provide some commentary on their January renewals, but the big four European reinsurers (Hannover Re, Munich Re, SCOR and Swiss Re, who together represent around one third of global P&C reinsurance premiums) provide more detail than their Bermudian and international peers. In this brief report, we examine the public disclosures from these companies, and have aggregated the four to present a composite picture.

For this group, some two thirds

of traditional treaty reinsurance premiums were up for renewal at

1 January 2020. Other important dates are 1 April (when Japanese and other

Asian business renews), 1 June (Florida cat) and 1 July (some US, Australasia

and other global programmes). Facultative and specialty business have no common

renewal dates and are spread throughout the year.

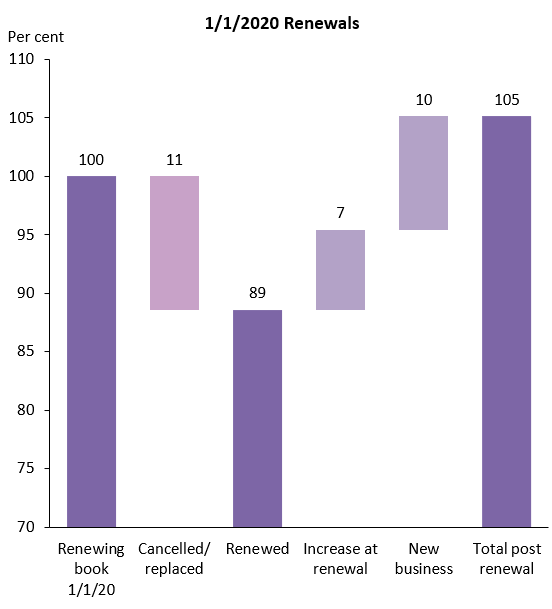

Combined result of 1 January renewals

Sources: company disclosures. Swiss Re reports in US dollars. For the purpose of this aggregation, its figures have been converted into euros using the 1 January 2020 exchange rate of USD 1 = EUR 0.892

We have combined the reported renewal experience of the four groups, and the overall picture is shown above. The development of the renewal is shown in the top waterfall chart. EUR 28.4bn of treaty reinsurance premiums were up for renewal. Of this 11% was cancelled or replaced[2], giving a total of EUR 25.2bn which was renewed. The 7% increase at renewal represents both the effect of price changes and increases in shares on treaties. New business contributed an additional 10%, benefiting from growth in core business lines. The combined portfolios grew 5%, compared with an increase of 12% at 1 January 2019, which was boosted by several non-recurring transactions at Swiss Re. Pricing was said to have firmed in many lines, especially in loss-affected business, but remained under pressure for non-loss-affected business classes and territories.

The overall rate and premium development at renewal reported by the four companies is presented in the bubble chart. Each of the groups reported an increase in premium rates ranging from 1.2% for Munich Re to 5.0% for Swiss Re. At 14%, Hannover Re reported the biggest growth in premium volume, while SCOR’s renewed premiums contracted 6%, reflecting portfolio management, particularly in China where substantial business was not renewed.

Hannover Re

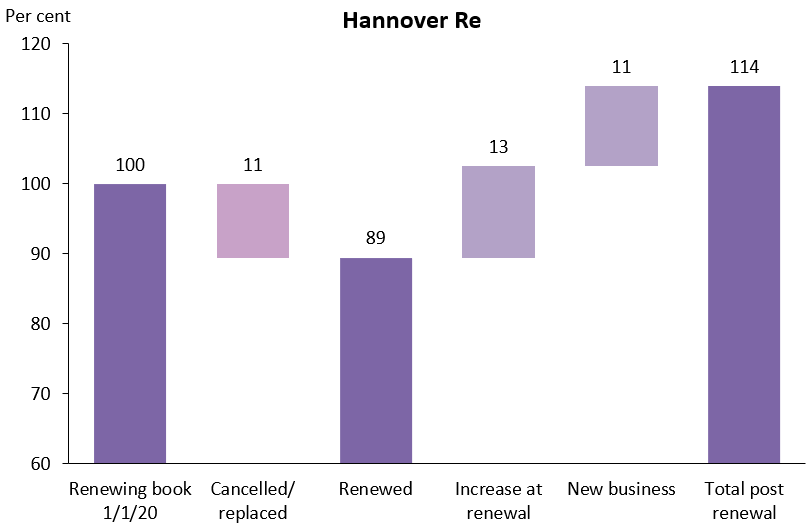

Hannover Re had EUR 7.0bn of traditional treaty reinsurance premiums up for renewal at 1 January 2020, representing 67% of its total book (excluding structured reinsurance, ILS and facultative). A further EUR 3.5bn is due to renew later in the year. Asia, Australia and the Middle East contributed 19% of renewing business, with 18% from North America, 17% from Germany, Switzerland, Austria and Italy, 17% from UK, Ireland and London Market, and 30% from the rest of the world. The renewal resulted in a 14% increase in premiums, driven by increased shares on existing business and substantial new business. The company said its underwriting was disciplined, strictly adhering to minimum margin requirements while business in excess of risk appetite was declined.

Hannover Re January 2020 renewals

Hannover Re noted that market capacity was sufficient and conditions continued to improve. Despite the withdrawal of some participants, traditional capacity continued to grow, while there was some tightening of the alternative capital market as capital remained trapped at the year-end because of uncertainty on assessment of recent large losses. Natural catastrophe pricing showed some hardening in the wake of recent loss experience, e.g. in the USA, and creep from prior years. However, Hannover Re identified Japan, Latin America and the Caribbean as regions where pricing was said to be still too low for the risk. The company said terms and conditions were slightly improved.

The volume of proportional business (75% of renewed premiums) grew by 15%, driven by growth in the underlying primary insurance market and new business acquired. Non-proportional premiums increased 10%, reflecting increased shares and new business gains.

Hannover Re reported growth in renewed premium across all major markets, ranging from 35% in Latin America, Iberian Peninsula and Agricultural business to 6% in Germany, Austria, Switzerland and Italy. Prices were increased by 2% for proportional business and 3% for non-proportional. Double digit rate increases were obtained on UK non-proportional motor, following the change to the Ogden discount rate. Natural catastrophe XoL premium increased by 10 % with pricing up 3%.

Munich Re

46% of Munich Re’s total P&C reinsurance book was up for renewal at 1 January 2020, with a focus on Europe, the USA (mainly excluding natural catastrophe which renews later in the year) and global business. EUR 10.2bn was up for renewal, resulting in EUR 10.7bn of renewed premiums, an increase of 4%. 31% of renewed premiums were derived from Europe, 28% Worldwide, 25% North America, 13% Asia/Pacific/Africa and 3% Latin America. Natural catastrophe business was 10% of the total. Business was expanded in in selected markets, driven particularly by specialty lines in Europe and Asia. Business which did not meet return criteria was sacrificed, e.g. Florida windstorm.

Munich Re January 2020 renewals

Casualty comprised 50% of renewed business, Property 32%, Marine 9%, Credit 5% and Aviation 3%.

Munich Re commented that premium rate trends varied among the different market segments in line with claims experience, with significant price increases in regions and classes subject to high claims experience, including the Caribbean and Aviation & Space. Conversely, rates were largely unchanged in regions and classes subject to low levels of recent loss activity, such as Europe and Asia (excluding Japan). Overall, a price increase of 1% was reported on the renewed book, ranging from +31% on Marine (9% of total) to a decrease of 6% on Property (22% of total). Munich Re said it increased prices for Property XoL by 11% overall, although the picture was said to be mixed with rate increases achieved on loss-affected business while pricing on loss-free accounts remained under pressure.

SCOR

Some two-thirds of SCOR’s book was up for renewal at 1 January 2020. At this time, 87% of the EMEA portfolio renews, 50% of the Americas and 56% of Asia-Pacific. A total of EUR 2.4bn of P&C Lines premiums were up for renewal. A further EUR 0.9bn of Global Lines[2] was subject to renewal but excluded from this analysis, showing an overall flat result. Renewed volume in P&C Lines were EUR 2.3bn, a decline of 6%, largely reflecting voluntary reductions on quota share business in China and the USA, which was only partly offset by firmer pricing and business growth elsewhere.

(P&C lines include: Property, Property Cat, Casualty, Motor & other related lines; Global lines include: Agriculture, Aviation, Credit & Surety, Inherent Defects Insurance, Engineering, Marine and Offshore, Space, Cyber, Motor Extended Warranty and inwards Retro.)

SCOR January 2020 renewals

SCOR said it obtained price increases across virtually all lines, except Agriculture (flat) and Credit & Surety (‑0.3%). Risk-adjusted pricing was firmer in virtually all territories, but there was some weakening in Asia-Pacific. The company said prices for proportional treaties increased by 2% overall (3% excluding China) and by 4% in non-proportional business. Renewed premium volumes fell 6% (2% excluding China) on proportional business as cedants retained more risk to capture positive evolution in primary business. Non-proportional renewed premiums were down 1%.

On a regional basis, EMEA renewals were flat, in the context of abundant capacity with pockets of rate hardening. In the Americas, renewed premiums were down 7% following portfolio management on short-tail lines and selective re-underwriting of casualty exposure. Renewing volumes were down 2% in Asia-Pacific (excluding China) but down 27% in total. The USA was the largest market for renewed business with EUR 747mn of gross premium, which declined 12%. Higher cedant retentions and portfolio management actions meant renewed premiums fell across virtually all business lines.

Swiss Re

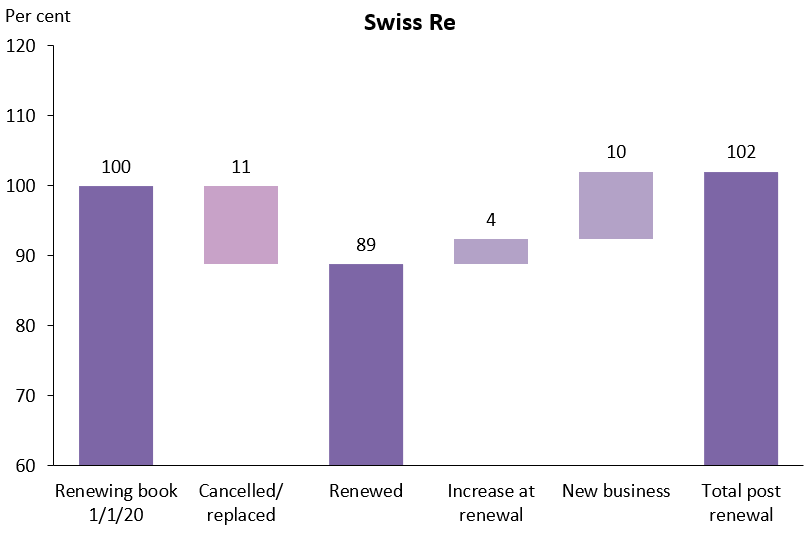

USD 9.8bn of Swiss Re’s treaty reinsurance premiums were up for renewal at 1 January 2020, with a reported outcome of USD 10.0bn, an increase of 2% (calculated from the movements disclosed by Swiss Re). This was in contrast to a 19% growth reported at 1 January 2019, which was heavily influenced by several non-recurring treaties. Growth was principally driven by natural catastrophe business. Overall, Swiss Re reported a 5% price increase.

Swiss Re January 2020 renewals

Swiss Re reported “favourable” rate increases on loss-affected natural catastrophe business which it has specifically targeted, resulting in a 14% growth in renewed premiums for this line. Rate increases across other classes were said to be more modest: Property (excluding nat cat) +3%, Specialty +8% while prices for Casualty were down 2% overall, despite strong rate increases for US XoL treaties. Price quality was said to be flat overall but still attractive, with sufficient rate increases to offset the negative impact of lower interest rates and higher loss assumptions. Terms and conditions were said to be stable. In response to market conditions, the economic capital deployed was overall unchanged, with +11% for non-proportional property nat cat business and -6% for casualty.

Casualty comprised 52% of renewed premiums, Nat cat and Property each 17% Specialty 14%. 49% of premiums were derived from EMEA, 36% from the Americas and 15% from Asia.

Leave a Reply