Why reinsurers should worry about cedant financial failure

Or “don’t buy the apartment without knowing the neighbourhood”

Yet just last year in the UK, two fairly high-profile primary carriers ceased underwriting due to financial duress, and the UK is not alone. Those of us with grey hair know the trail of problems that can leave behind, although, of course, mostly for policyholders and brokers.

Why should reinsurers care?

It’s fair to say that it depends on the reinsurer’s relationship with the cedant, but I would contend that it’s always important, and gets more important the closer the reinsurer is to ‘following the fortunes’. In other words, if you’re writing their long-tail Quota Share, it should be highly important; if you’re just at the top end of the cat programme, less so.

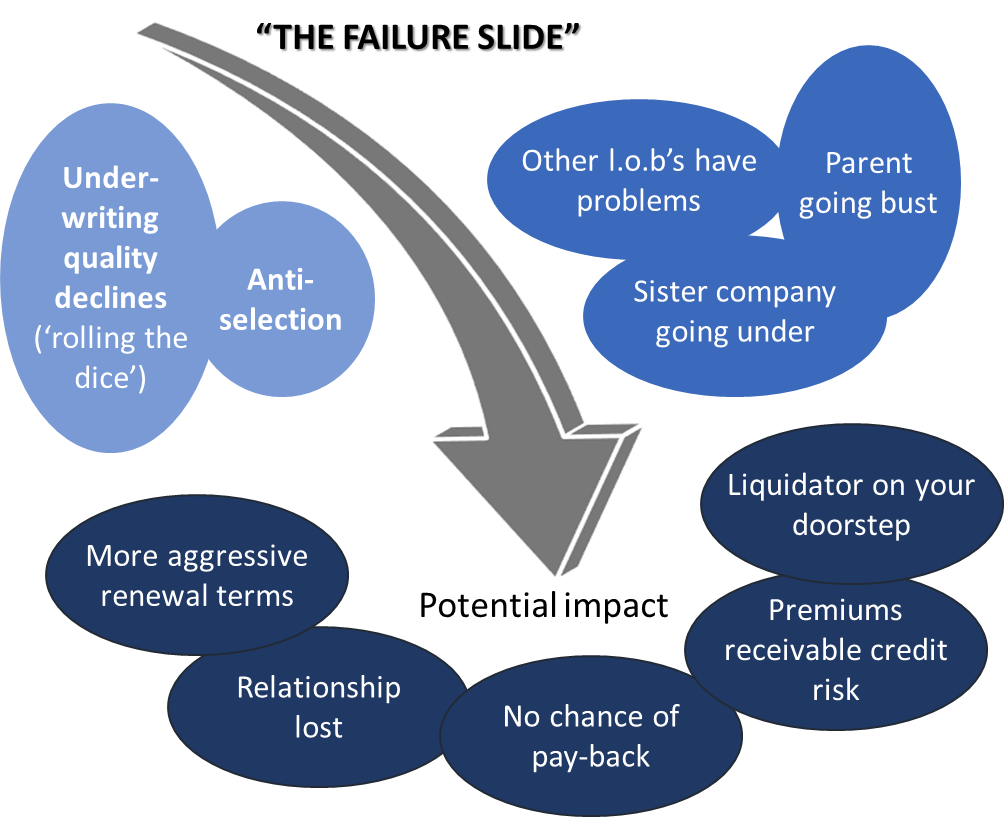

Reinsurance underwriters tend to focus largely on the risk(s) they see. If they’re lucky, they’ll see offerings across the board, which should at least give them some idea of what the overall business looks like. Even then they won’t be looking at the broader financials or those of mother or sister companies, or have a sense of the probability of survival of the overall business. However there have been many occasions when the sister company or parent has failed and brought the whole business down with it. So the underwriter’s a bit like a knee surgeon doing the operation without checking that the patient’s heart is up to it.

Old school theory has it that when an insurer is under pressure, it may start compromising on underwriting – trying to write their way out of the problem – and senior management pressure may push an otherwise sensible business in that direction. Historically well-performing treaties may be undermined by this. Equally, when issues are apparent externally, their policyholders or brokers may become more selective in the business they offer to them.

Any or all of these can lead to a ‘failure slide’, starting with writing for income and aggressive renewal negotiations. Then if/as/when they go out of business, the investment in building the relationship is lost, any chance of pay-back has probably gone, the credit risk in terms of premiums receivable increases, and ultimately you might find the liquidator on your doorstop insisting you settle outstanding claims even though you haven’t had the premium.

My advice would be that if you want to buy the apartment, check out the neighbourhood…

Peter Hughes

Managing Director

September 2017

Leave a Reply